In today’s uncertain economic climate, having a financial safety net in place is essential. An emergency fund can provide peace of mind and financial stability during unexpected situations. This blog will guide you through the process of building an emergency fund quickly in Ireland, focusing on practical steps and management tips to help you reach your goals. Ready to secure your financial future? Let’s dive in!

What is an Emergency Fund?

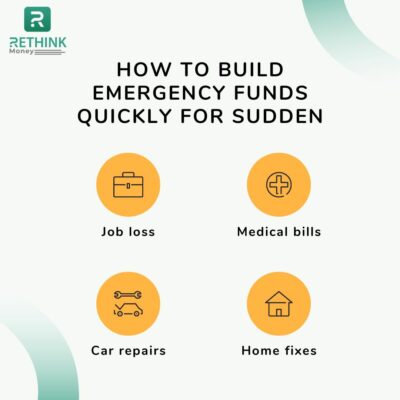

An emergency fund is a dedicated financial reserve specifically set aside to provide a safety net in the event of unforeseen circumstances or financial emergencies. These emergencies can range from unexpected medical expenses and car repairs to a sudden job loss or other significant life events. By having an emergency fund in place, individuals can effectively manage the financial impact of these situations without resorting to debt or drastically impacting their long-term financial plans. In essence, an emergency fund acts as a financial buffer, offering stability and peace of mind during challenging times.

Why is an Emergency Fund Important?

An emergency fund is crucial for several reasons:

- It reduces stress by providing a sense of financial security.

- It prevents you from relying on credit cards or loans during emergencies, which can lead to long-term debt.

- It allows you to focus on resolving the emergency itself rather than worrying about finances.

Setting Emergency Fund Goals

Assessing Your Financial Situation

Before you start building your emergency fund, carefully asses your current financial situation. Calculate your monthly expenses and outstanding debts to understand how much fund you need to build.

Determining Your Emergency Fund Target Amount

A general rule of thumb is to save three to six months’ worth of living expenses in your emergency fund. However, this may vary depending on your financial situation and risk tolerance. Consider factors such as job stability, family size, and existing financial obligations when determining your target amount.

Practical Steps to Building Your Emergency Fund Quickly

Create a Budget

To start saving, create a detailed budget that includes all your income sources and expenses. This will allow you to identify areas where you can cut costs and allocate more money towards your emergency fund.

Cut Unnecessary Expenses

Review your budget and identify non-essential expenses that can be reduced or eliminated. For example, consider cutting back on impulse purchases, subscriptions, or dining out. Redirect the money saved towards your emergency fund.

Increase Your Income

Look for opportunities to increase your income, such as taking on freelance work, getting a part-time job, or selling items you no longer need. Use this extra income to boost your emergency fund contributions.

Automate Your Savings

Set up automatic transfers from your main account to your emergency fund. This will help you stay consistent and disciplined in your savings efforts.

Open a Dedicated Savings Account

Open a separate savings account specifically for your emergency fund. This will help you avoid the temptation to dip into your savings for non-emergency expenses.

Use Windfalls Wisely

Unexpected windfalls, such as tax refunds, work bonuses, or inheritances, can provide a significant boost to your emergency fund. Instead of spending this extra money, consider using it to reach your savings goal more quickly.

Managing Your Emergency Fund

Monitor Your Progress

Regularly review your emergency fund’s progress, comparing it to your target amount. It will keep you motivated and allow you to make adjustments as needed.

Reassess Your Goals

As your financial situation evolves, your emergency fund goals may need to be adjusted. Periodically reassess your target amount and make changes if necessary.

Keep Your Emergency Fund Accessible

Choose a savings account that allows easy access to your funds without penalty. This ensures that you can quickly access your money in case of an emergency.

Our Advice

We understand the importance of having a solid financial foundation. Therefore, we highly recommend establishing an emergency fund for our clients as a crucial aspect of their overall financial plan. Please consider these two pieces of advice when building and maintaining an emergency fund:

- Prioritise your emergency fund: Saving for an emergency fund should take precedence over non-essential spending and even some long-term savings goals. Having a financial safety net can prevent debt and financial stress in the long run.

- Stay disciplined: Building an emergency fund takes time and discipline. Stay focused on your goals, and regularly review and adjust your financial plan as necessary.

Remember, having an emergency fund is an essential part of a healthy financial plan. By following the advice outlined in this section, you can work towards creating a financial safety net that will provide you with peace of mind and stability in the face of life’s unexpected challenges. Contact us if you need a free personalised financial plan.

FAQ

Is it better to pay off debt or save for an emergency fund first?

Prioritise establishing a small emergency fund to cover minor unexpected expenses. Once you have this, focus on paying off high-interest debt, then work on building your full emergency fund.

How can I save for an emergency fund if I live pay check to pay check?

Start by creating a budget, cutting non-essential expenses, and looking for ways to increase your income. Even small contributions to your emergency fund can add up over time.

What type of account should I use for my emergency fund?

Choose a savings account with a competitive interest rate, no fees, and easy access to your funds in case of an emergency.

Should I invest my emergency fund?

Investing your emergency fund is generally not recommended, as it should be easily accessible and not subject to market fluctuations.

Can I use my emergency fund for non-emergency expenses?

Avoid using your emergency fund for non-emergency expenses, as this can leave you vulnerable during an actual emergency. If you need to dip into your fund, replenish it as soon as possible.

What is the difference between rainy-day funds and emergency funds?

Rainy day funds are designed to cover smaller, less urgent expenses, such as minor home repairs or replacing a broken appliance. On the other hand, emergency funds are meant for more significant, unexpected financial crises, such as job loss or medical emergencies. Having both types of funds in place is a good idea to ensure you’re prepared for any financial challenge.